In late April, the CBOE started a new index, the CBOE 1-Day Volatility Index (VIX1D), that tracks the implied volatility of one-day S&P 500 options. Like the VIX index, which has been tracking the 30-day implied S&P 500 options volatility since 2003, the 1-day VIX provides a picture of the equity market’s perceptions of risk, but over a much shorter period. The 1-day VIX index is a step forward in democratizing financial data, providing useful clues on short-term market sentiment and allows investors to easily compare volatility across time periods. However, the increasingly popular 0DTE (zero days-to-expiration) options that make the index possible, seem as if they should exist in the world of gambling rather than investing.

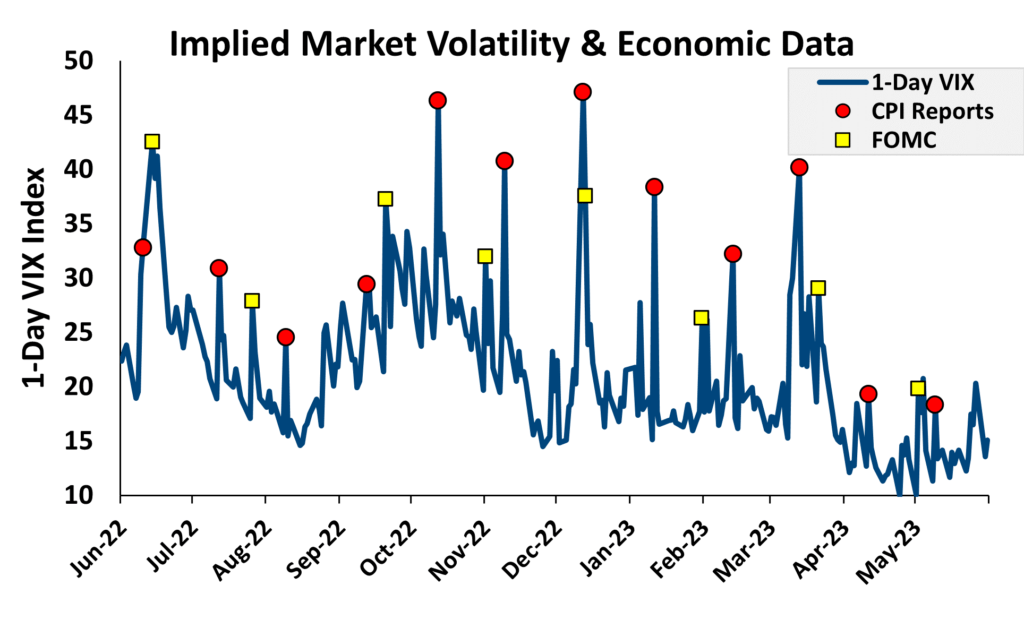

As an example of a positive use case for the 1-day VIX index, data from this year shows that the level of market concern surrounding macro-economic risks is easing. Prior to April, daily volatility spiked around CPI (inflation) and FOMC rate announcements, as the stock market was worried about the impact of higher interest rates on stock prices. However, in the last couple of months, 1-day bets on market moves around the days of these economic releases have been pricing in lower implied volatilities, indicating that the market is less concerned about inflation and rates.

On the gambling aspects of 0DTE options, according to JP Morgan, the notional value of daily trading in 0DTE options is near $1 trillion. The CBOE estimates that 46% of total options trading volume occurs in contracts with less than 5-days until expiration. Academics are theorizing that growth in the usage of these contracts could increase underlying market volatility.1. Another paper estimates that retail traders, on average, lost $358,000 per day trading 0DTE options.2.

As advisors who believe in building robust, long-term oriented portfolios, we do not see much utility for institutional investors in participating in the 0DTE options market; it is hard to see a need to hedge 1-day market moves. However, the more specific information that the one-day options provide on daily volatility and the relative importance markets are placing on events is useful for information purposes and assessing sentiment.

1. Brogaard, Han, & Won. How Does Zero-Day-to-Expiry Options Trading Affect the Volatility of Underlying Assets?

2. Beckmeyer, Branger, and Gayda. Retail Traders Love 0DTE Options… But Should They?