In most fields, there are fundamentals upon which the discipline relies, for example, the four fundamental forces in physics. In investing and finance, the risk-free rate (i.e., the interest rate on three-month Treasury Bills) is one such fundamental. The risk-free rate represents the rate of return an investor can expect to earn if they take no risk. The capital asset pricing model, Sharpe ratio, options pricing formulas, and most financial models use the risk-free rate as an input. The problem at hand is that short-term Treasuries bills do not appear to be risk-free right now.

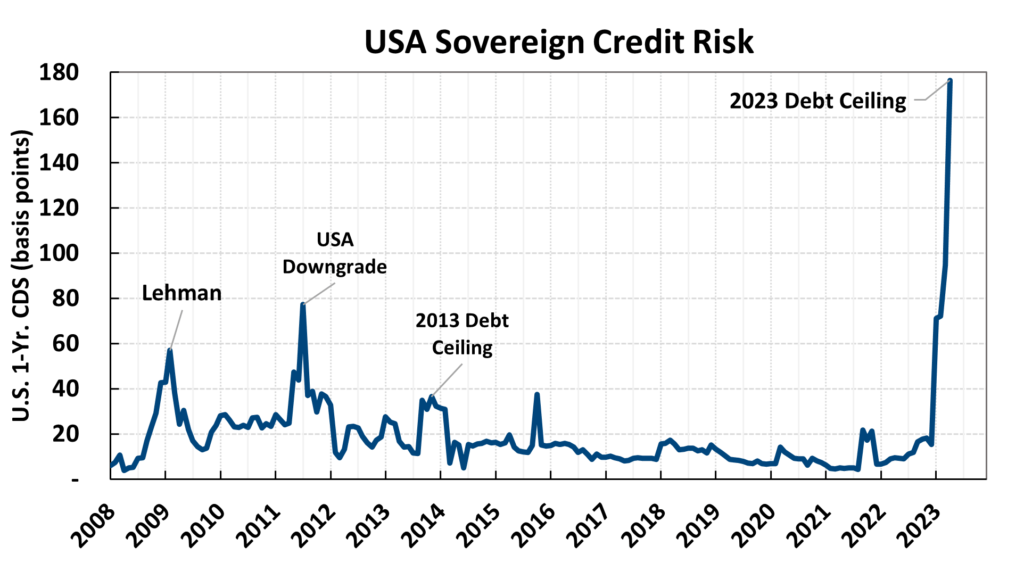

As the chart shows, the cost to buy protection against a U.S. Treasury default is at its highest level since the invention of sovereign bond credit default swaps (CDS). Looking at short-term Treasury yields, T-Bills maturing in the summer months are yielding about 100 basis points more than T-Bills maturing in May, and trailing 2-year realized Treasury volatility is approaching 2008 levels. According to the World Gold Council, central banks have been increasing their gold reserves. All these factors indicate that the market is expecting a very contentious struggle to increase the U.S. statutory debt limit.

In the era of modern finance, the only major stress period rooted in the willingness / ability of the U.S. Government to pay bond holders was in the summer of 2011. After a contentious agreement was reached to raise the debt limit in July, S&P downgraded the U.S. credit rating to AA+. The market reaction was counterintuitively to buy Treasuries and to sell higher risk assets. Investors soon forgot about the downgrade and stocks and bonds both rallied for years to follow.

If investors can’t be sure about the “safest asset in the world,” then the range of expected short-term investment outcomes to consider is much wider than usual. Mortgages and high-quality investment-grade credit may provide both a better yield and less realized volatility than Treasuries this summer. If a compromise can nullify the debt limit risk, it could stoke a relief rally for risk assets. However, if a compromise does not materialize, the market could react as it did in 2011. In summary, we are open to thinking about outcomes which seem unlikely or even impossible.